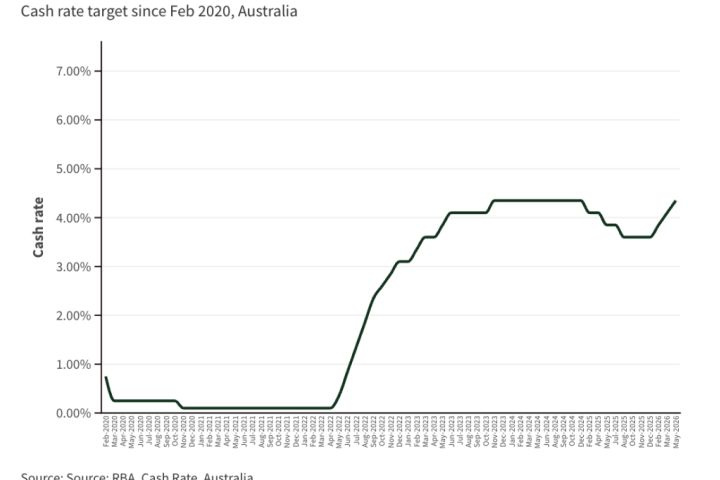

Interest rates have been on a rollercoaster ride over the past few years, and 2026 is proving no different. With the Reserve Bank of Australia (RBA) adjusting the cash rate in response to inflationary pressures and global economic shifts, mortgage brokers are playing a crucial role in helping clients make informed decisions.

For many Australians, even a small change in interest rates can have a big impact on household budgets. As a broker, your ability to guide clients through these fluctuations can build trust, strengthen relationships, and position you as a long-term financial partner.

Understanding the Current RBA Landscape

As of mid-2026, the RBA has maintained a cautious approach, keeping the cash rate in a range designed to balance inflation control with economic growth. While rates are lower than the peaks of 2023, they remain higher than the historic lows seen during the pandemic.

This environment means borrowers need to be strategic — and brokers need to be proactive in offering tailored solutions.

Fixed vs Variable Loans: Helping Clients Choose Wisely

One of the most common questions clients ask during periods of rate volatility is whether to lock in a fixed rate or stick with a variable loan.

Fixed Rate Loans

- Provide certainty in repayments for a set period (usually 1–5 years)

- Protect clients from sudden rate hikes

- May come with break fees if paid out early

Variable Rate Loans

- Offer flexibility and often allow extra repayments without penalty

- Can benefit clients if rates drop

- Carry the risk of higher repayments if rates rise

Broker Tip:

Encourage clients to consider a split loan — part fixed, part variable — to balance stability with flexibility. This can be particularly appealing in uncertain markets.

Refinancing Opportunities

Interest rate changes often open the door to refinancing opportunities. Clients who locked in higher rates in previous years may now benefit from switching to a more competitive product.

Key Refinancing Strategies:

- Review client loans annually to ensure they remain competitive

- Consider debt consolidation to simplify repayments and reduce interest costs

- Explore offset accounts to help clients reduce interest while maintaining liquidity

Example in Australia:

Some brokers are using AI-powered comparison tools to quickly identify better loan options for clients, factoring in fees, features, and repayment flexibility.

Proactive Client Communication

In volatile markets, silence can create anxiety. Regular, clear communication reassures clients that you’re monitoring their situation and ready to act if needed.

Best Practices:

- Send quarterly rate update emails summarising RBA decisions and market trends

- Offer personalised loan health checks after significant rate changes

- Use plain language to explain complex financial concepts

Example:

A broker who sends a short video update after each RBA announcement can stand out as a trusted advisor, even if no immediate action is required.

Positioning Yourself as a Long-Term Partner

Helping clients navigate interest rate changes isn’t just about the numbers — it’s about building relationships. By offering ongoing support, you position yourself as more than a transaction facilitator; you become a financial guide.

In 2026, the brokers who thrive will be those who combine market knowledge with empathy, ensuring clients feel confident and informed no matter what the RBA decides.