Secret – It’s not Tax incentives

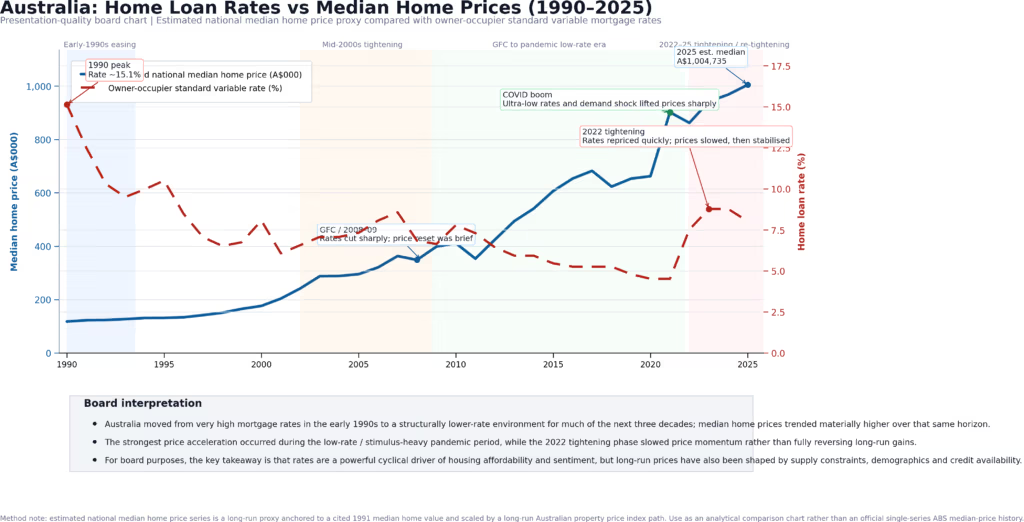

Across the 1990–2025 period, Australian property prices rose through multiple booms, slowdowns and resets. Tax settings such as negative gearing and the CGT discount often get the spotlight, but a calmer, credit-focused view suggests the bigger, more consistent forces were:

- the long downtrend in interest rates (and the borrowing-power effect)

- persistent housing supply constraints (including infrastructure and delivery capacity)

- population growth increasing underlying demand

That doesn’t mean tax incentives had no impact. They likely contributed at the margin for some investors. But over the long run, interest rates and supply-demand fundamentals are the more direct, economy-wide explanation.

Why the interest-rate backdrop matters (1990–2025)

The RBA cash rate sets the tone for borrowing costs in Australia. While lenders price mortgages based on more than the cash rate alone, the broad direction matters: from the early 1990s (high rates by today’s standards) to the record-low environment around 2020–2021, the trend was down.

Lower rates don’t just make existing loans cheaper. They change what buyers can afford to pay for a property, which is where prices are set.

Borrowing power: the bridge between rates and prices

For mortgage professionals, the key mechanism is borrowing power (also called borrowing capacity): the maximum a lender may advance based on income, expenses, liabilities and policy.

Lenders also test serviceability using buffers—assessing repayments at a higher “what if rates rise?” level. Even with buffers, lower actual rates can increase the loan size a household can qualify for.

A simple illustration:

- With a $5000 monthly repayment budget, at 7% you might borrow around $755,000.

- At 4%, the same repayment budget might support around $1,050,700. (Actual rate not Servicing rates)

When many buyers experience that uplift at once, it can lift the market’s price ceiling—especially where listings are tight.

Where negative gearing and the CGT discount fit

Two common investor tax settings are:

- Negative gearing: when investment costs exceed rental income, and the loss can offset taxable income.

- CGT discount: a reduced tax rate on capital gains for assets held long enough.

These can improve after-tax returns and influence investor participation. But their reach is narrower than rates:

- rates affect owner-occupiers and investors

- tax settings mainly affect investors, and their impact depends on income, expectations and credit availability

So while tax incentives can shape who buys and when, they’re less likely to be the primary driver of nationwide price growth over decades.

Supply, infrastructure, and population: the structural squeeze

Australia’s housing market has also faced long-running constraints:

- slow planning and approval pipelines

- construction capacity limits and cost pressures

- infrastructure timing (transport, utilities, schools) affecting where supply can expand

At the same time, population growth and migration increased demand—especially in Sydney and Melbourne, with flow-on effects to key regional markets.

This helps explain why prices can rise even when rates rise: if supply is tight enough, demand can still outbid available stock. And it explains why prices can stall even when rates fall: if lending tightens, recession risk rises, or sentiment drops, buyers may step back.

Disclaimer: This article is general information only and does not consider individual circumstances. Consider speaking with a licensed mortgage broker and a qualified tax adviser before acting.

Conclusion

Over 1990–2025, the broad-based downtrend in rates—and the resulting increase in borrowing power—was the strongest, most direct driver of higher Australian (and international) property prices. Add constrained building supply, infrastructure bottlenecks and population growth, and you have a more complete explanation than tax incentives alone.

If you’re advising clients, talk them through scenarios:

- review borrowing power under different rate paths

- compare variable vs fixed options

- build a buffer for future rate changes

accreditedbroker.com.au can help you model the numbers and plan the next move.

FAQ’s

1) Did falling interest rates really push property prices up?

Yes in many periods, lower rates reduced mortgage repayments and increased borrowing power, allowing buyers to bid more for the same homes. Over time, that can lift market-wide prices, especially when listings are tight.

2) What do you mean by borrowing power?

Borrowing power (borrowing capacity) is the approximate maximum a lender may be willing to lend based on income, expenses, existing debts and lending policy. When rates fall, the same repayment budget can often support a larger loan.

3) If rates are the main driver, do negative gearing and the CGT discount matter at all?

They can matter, particularly for investor behaviour and after-tax returns. The point of the article is that theyre typically secondary influences compared with interest rates, credit conditions, supply constraints and population growth.

4) How does the RBA cash rate affect home loan rates?

The RBA cash rate influences funding costs across the financial system. Lenders then set variable and fixed mortgage rates based on that backdrop plus wholesale funding markets, competition and risk settings.

5) Why can prices rise even when interest rates rise?

Because prices are also driven by supply and demand. If housing supply is constrained (planning delays, construction capacity, infrastructure timing) and demand remains strong (jobs, wages, migration), prices can stay resilient even with higher rates.

6) Why can prices stall even when interest rates fall?

Rate cuts don’t guarantee stronger prices. If lenders tighten serviceability, if buyers worry about job security, or if sentiment is weak, demand can soften even in a lower-rate environment.

7) What’s the key takeaway for brokers and advisers?

Focus client conversations on the big levers:

- model borrowing power under different rate scenarios

- stress-test mortgage repayments and cash flow

- compare variable vs fixed options

- encourage buffers for future rate changes

8) Is this advice?

No. This is general information only and doesn’t consider individual circumstances. Clients should speak with a licensed mortgage broker and a qualified tax adviser before acting.