If you’ve been watching Australia’s economy lately and feeling a strange sense of familiarity, you’re not imagining it. The mix of heavy government spending, stubborn inflation, and a central bank trying to thread the needle has a “we’ve seen this movie before” vibe.

This article isn’t about panic. It’s about pattern recognition—because in finance, the biggest mistakes often come from assuming “this time is different” without doing the comparison.

1) Which party was in government then—and now?

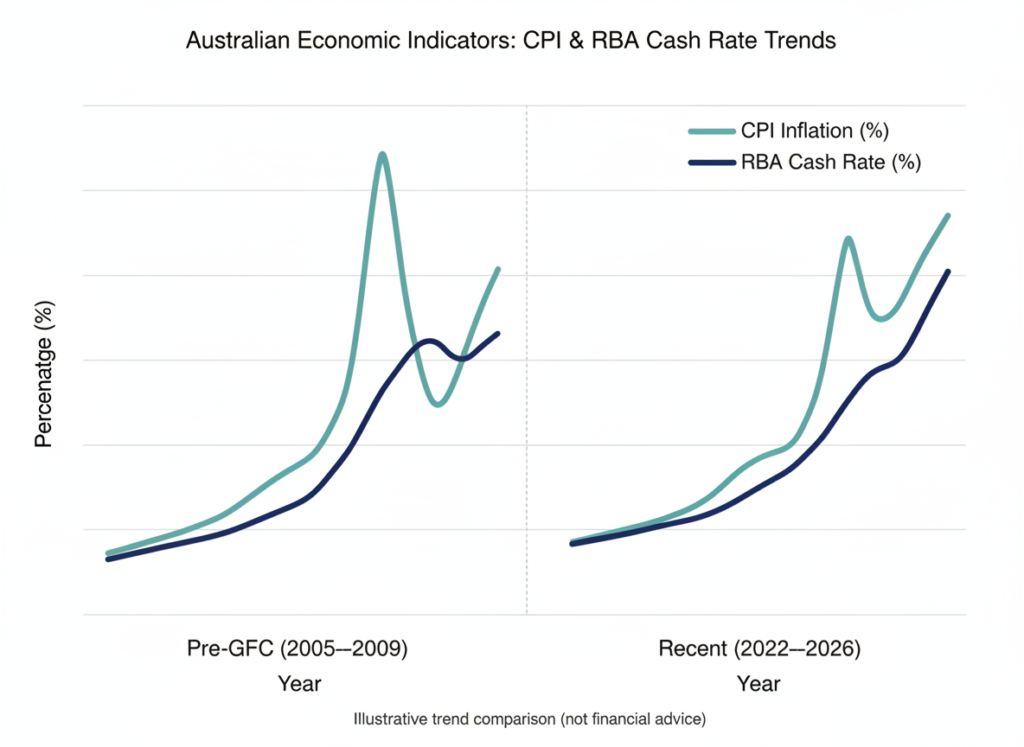

In 2007, Australia was governed by the Australian Labor Party (ALP) under Kevin Rudd (elected in late 2007). Today (2026), Australia is again governed by the ALP.

The point isn’t that one party “causes” a crisis. The point is that policy settings—especially spending and regulation—shape inflation, interest rates, and confidence.

2) What were their policies?

2007-era settings (pre-GFC)

In the lead-up to the GFC, Australia benefited from a strong resources boom and rising household wealth. But the economy was also running hot.

Key themes included:

- Strong domestic demand and consumer confidence

- High credit growth and a housing market supported by easy access to finance

- Government policy settings that, in combination with private-sector borrowing, contributed to an economy operating near capacity

Current settings (2026)

- Large-scale government spending programs and ongoing structural deficits

- Cost-of-living pressure and inflation that has proven harder to “put back in the box”

Fast-forward to today and the themes rhyme:

- A policy environment that often aims to cushion households from economic pain—helpful in the short term, but inflationary if it keeps demand elevated

The common thread: when spending (public and private) runs ahead of the economy’s ability to supply goods and services, prices rise.

3) What was the Reserve Bank doing?

Then

In the mid-2000s, the Reserve Bank of Australia (RBA) was tightening monetary policy to contain inflation. Rates were lifted as the Bank tried to cool demand without derailing growth.

Now

Today, the RBA has also been in a tightening cycle (or maintaining restrictive settings) to fight inflation. The dilemma is similar:

- Raise rates to slow inflation

- But risk damaging growth, employment, and household cash flow

For brokers and borrowers, the practical reality is the same: when inflation is the problem, interest rates stay higher for longer.

4) What was the world economy doing?

Then

In 2007, the global economy looked strong on the surface:

- Solid growth in the US and Europe (until cracks widened)

- China’s rapid expansion supporting commodity demand

- Global credit markets flush with liquidity

But underneath, leverage was building—especially in the US housing and structured credit markets.

Now

The global economy today also has a “strong on the surface, fragile underneath” feel:

- Higher global interest rates after a long era of cheap money

- Elevated government debt levels across many developed economies

- Ongoing geopolitical and supply-chain risks

Different triggers, similar vulnerability: when the system is highly leveraged, shocks travel faster.

5) What happened to the financial markets?

Then

In 2007, markets went from calm to chaotic as credit risk was repriced:

- Liquidity dried up

- Risk premiums blew out

- Equity markets rolled over

- Funding costs surged for banks and non-bank lenders

Now

We’re again in a period where markets are highly sensitive to:

- Inflation prints

- Central bank commentary

- Government budgets and debt issuance

When confidence is fragile, markets don’t need a “big” event—just a catalyst.

6) What happened to confidence?

Confidence is the invisible engine of credit.

Then

Once people realised the risks were bigger than advertised, confidence collapsed:

- Consumers pulled back

- Businesses delayed hiring and investment

- Lenders tightened credit standards

Now

Confidence today is being tested by:

- Cost-of-living stress

- Mortgage repayment pressure

- Uncertainty about the path of rates

- A sense that “the rules keep changing” (tax, regulation, incentives)

When households feel squeezed, they stop spending. When lenders feel uncertain, they stop approving.

7) What was the result?

In 2007–2009, the result was a global credit crunch and a sharp repricing of risk. Even where Australia avoided the worst of the recessionary impact, the lending landscape changed:

- Tighter servicing and documentation

- Higher funding costs

- Greater scrutiny of borrower quality

The big lesson: credit is always available—until it isn’t.

8) What’s likely to be the future?

No one can time the next crisis perfectly. But we can outline plausible scenarios.

Scenario A: “Soft landing” (best case)

- Inflation gradually falls

- Rates ease slowly

- Employment holds up

- Property markets stabilise rather than surge

Scenario B: “Higher for longer” (most likely if inflation sticks)

- Rates remain restrictive

- Household cash flow stays pressured

- Credit growth slows

- Business failures rise modestly

Scenario C: “Confidence shock” (the GFC-style risk)

This is the one that feels most like 2007:

- A trigger event hits (global recession, funding stress, geopolitical shock, or a sharp asset-market correction)

- Lenders reprice risk quickly

- Credit availability tightens

- Borrowers with thin buffers get caught

What brokers (and borrowers) should do now

Whether or not history repeats exactly, preparation beats prediction.

- Stress-test borrowing capacity: Assume rates stay higher longer than you’d like.

- Prioritise buffers: Offset accounts, redraw, emergency funds.

- Review loan structure: Fixed vs variable splits, IO vs P&I, and expiry cliffs.

- Watch lender policy shifts: Credit appetite changes before headlines do.

- Get proactive advice: The best outcomes are engineered early, not negotiated late.

Final thought

“Déjà vu” doesn’t mean we’re guaranteed a repeat of the GFC. But it does mean the ingredients—spending, inflation, tightening, and fragile confidence—are familiar.

If 2007 taught us anything, it’s that markets don’t break when everyone is scared. They break when everyone is comfortable.